Cracking the Code: Why Breaking into UK Off-Licence Retail is So Difficult for New Brands

Entering the UK off-licence and retail market is no small feat. For emerging food, beverage, and alcohol brands, the barriers to success are as steep as they are often invisible — financial, structural, regulatory, and behavioural. While the promise of visibility and volume in independent retail exists, the reality is a fragmented, competitive, and risk-averse marketplace where brand survival is often measured in months, not years.

RETAIL

Anil Junagal

7/26/20252 min read

The Real Cost of "Getting on Shelf"

It’s a common misconception that if your product is good, it will sell. In reality, entering the UK retail ecosystem — particularly in the off-licence and convenience store segments — requires substantial capital before a single unit moves.

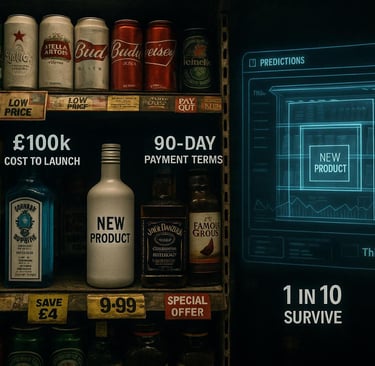

Initial listing fees with wholesalers or retailers can exceed £2,000 per SKU.

POS marketing kits, shelf talkers, and merchandising often add £5,000+ to launch budgets.

Initial production runs and compliance documentation can drain £50,000 to £100,000 — easily.

These upfront costs rarely include the promotional allowances or buy-back guarantees many retailers demand. It’s a gatekeeping structure that naturally filters out undercapitalised but potentially innovative brands.

Distribution: Built on Relationships, Not Just Merit

Distribution isn’t just about logistics — it’s political. The wholesalers that supply thousands of off-licences across the UK prefer brands they know, trust, and have a proven sales history with. That often excludes new entrants.

Retailers, especially independents, depend on their limited shelf space to deliver consistent turnover. Listing an unknown product is risky when a space could otherwise stock a guaranteed seller.

Without leverage, new brands often face:

Refusal to stock, regardless of product quality.

Demand for upfront marketing budgets before the first order.

Long payment cycles — 60 to 90 days is standard — that worsen cash flow strain.

Regulation and Retail Reality

The UK's regulatory landscape is not forgiving. From AWRS registration and alcohol licensing to health warnings and age-verification compliance, alcohol and F&B brands are tightly policed. Non-compliance — even unintended — can lead to product removal or hefty fines.

And even once legal boxes are ticked, brands face the other reality: consumers are now more value-driven than ever. In 2024, over 77% of UK consumers said they would choose value over brand loyalty. With private label products dominating shelf space and discount retailers expanding market share, convincing someone to spend more on something new is an uphill battle.

A Market Saturated — and Skeptical

Over 30,000 consumer products launch globally every year. In the UK, off-licence operators face constant pitch fatigue from emerging brands vying for attention. Most products fail to stand out, and those that do often struggle to sustain volume without constant promotional support.

The result? Only one in ten alcohol brand launches survives beyond 24 months.

Where ThirdRetail Fits

While the landscape is challenging, there are models working to reduce friction for both brands and retailers. Platforms like ThirdRetail are designed to make product discovery and retail matchmaking more efficient. Instead of navigating blind pitches and uncertain ROI, retailers can access brand data, demand forecasts, and shelf performance predictions — all before a product hits the shelf.

For new brands, this means:

Smarter targeting of retail locations that match their audience.

Lower entry risk through data-driven placement rather than costly trial-and-error.

Improved cash flow by accessing stores more open to new offerings with evidence-backed decisions.

Though platforms alone can't eliminate systemic barriers, they can make market entry more transparent and opportunity-based.

Conclusion

The barriers to entry in UK off-licence retail are real — and growing. Capital constraints, retailer conservatism, regulatory hurdles, and shifting consumer priorities all conspire to make launching a new product incredibly hard.

Yet innovation isn’t dead. It’s just hidden behind walls that need dismantling. As smarter tools emerge to connect brands and stores more meaningfully, there’s renewed hope that future success won’t depend on budget alone — but on relevance, fit, and data-led decisions.

Strategy, operations, and digital transformation for modern enterprises.

Info@junagal.com

© 2025. All rights reserved.